Why traditional portfolios are being tested

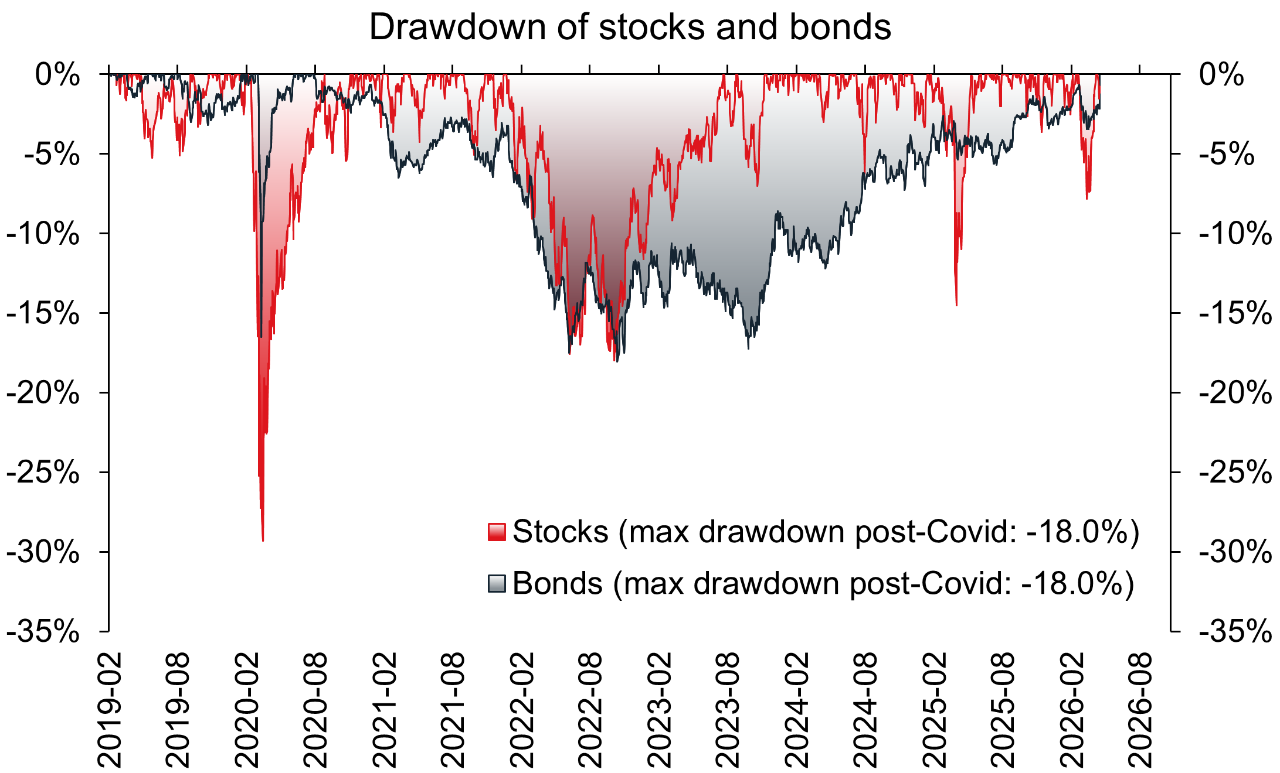

For a long time, building a portfolio was relatively straightforward: stocks for growth, bonds for stability. But recent years have shown that stocks and bonds can decline at the same time, market volatility can show up suddenly and last longer and economic outcomes are harder to predict.

Traditional portfolios are not broken, but diversification beyond stocks and bonds matters more than ever, leading many investors to liquid alternatives.

Source: NBI and Refinitiv. For Illustrative purposes only.

What are liquid alternatives?

Liquid alternatives are investment strategies designed to behave differently from the stock and bond markets, while still being easy to buy and sell.

Many liquid alternatives are offered as an ETF or mutual fund and offer key features such as daily liquidity, transparency and are designed to manage risk. They don’t rely solely on markets going up to make money and that can be valuable when markets are choppy.

Why liquid alternatives make sense now

Liquid alternatives make sense in today’s markets because conditions are more uncertain and less forgiving than they were for much of the past decade. Interest rates have moved higher and stayed there longer as central banks continue to manage inflation, increasing bond volatility and reducing their ability to consistently offset equity losses.

Markets have also become more reactive, with economic data, policy signals, and geopolitical events triggering frequent and sudden price swings. Instead of steady trends, investors now face sharper drawdowns and less predictable recoveries.

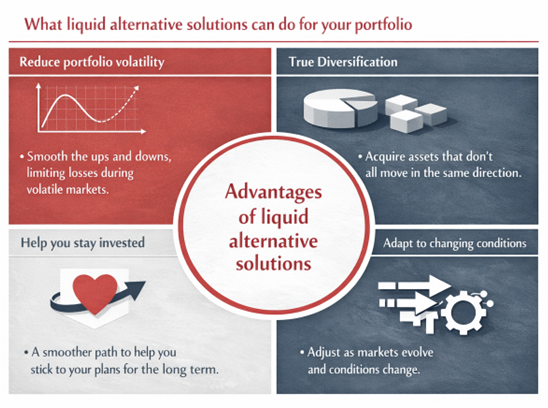

What liquid alternatives can do for a portfolio

1. Reduce portfolio swings

Liquid alternatives aim to smooth out ups and downs. They may not deliver big gains in strong bull markets, but they can help limit drawdowns when markets struggle.

2. Add real diversification

True diversification means owning assets that don’t all move together. Many liquid alternatives follow different return drivers, such as market trends, relative pricing, or defensive positioning.

3. Help you stay invested

Large portfolio losses can lead to emotional decisions. A smoother ride can make it easier for investors to stick with their long term plan.

4. Adapt to changing conditions

Some liquid alternative strategies adjust exposure as markets evolve, rather than staying fully invested regardless of risk.

The bottom line

For many investors, liquid alternatives can be a practical way to strengthen a portfolio. They add enhanced diversification beyond stocks and bonds, help navigate market volatility more thoughtfully, and support a portfolio that is better prepared for uncertainty. While they do not fully eliminate risk, liquid alternatives are designed to help manage it more effectively, especially in markets like today’s.